Startups are Risk Bundles

Startup founders are sometimes surprised when they spend a year or two executing against their roadmap, make a lot of progress, and still have to struggle to raise more capital. Why wouldn’t investors be interested in a company if it’s much further along than it was last year? Why are the few investors who are interested only willing to invest at a lower valuation?

Unfortunately, all progress is not created equal. Sometimes moving forward gets founders closer to the goal of building a huge, profitable company, but sometimes it shows that they’re on the wrong path, or that their goal is unattainable.

A bundle of risks

In order to understand if a startup is making meaningful progress, it’s useful to analyze it as a bundle of risks that must eventually be addressed. Here are a dozen sample startup risks:

Can the founders work well together? (What if the team starts breaking up at the first sign of trouble?)

Do the founders have the complementary skills required for realizing the startup’s vision? (What if a startup needs a world-class machine learning expert, but none of cofounders are great at machine learning?)

Can the team build a great product? (What if the founders are just out of college and don’t have a portfolio of past work that demonstrates their potential?)

Will the team be able to find product-market fit? (What if the CEO is fixated on a specific product idea and wants to build it without getting feedback from potential users?)

Can the founders manage growing teams of people? (What if they don’t have any management experience? What if they seem abrasive?)

Will target customers be willing to pay a healthy price for the product? (What if customers love the product but are only willing to pay a little bit because of low budgets or the presence of cheap substitutes?)

Is the sales cofounder good enough at selling? (What if the sales cofounder is actually an engineer who wants to try their hand at sales, or a salesperson who only has experience selling much cheaper products?)

If the startup takes off, will others just copy the idea? (What if there aren’t any clear barriers to entry, and no durable competitive advantages?)

Will churn be manageable? (What if a company is targeting a set of customers that go out of business frequently, like SMBs?)

Is the company fundable by investors? (What if it’s in a gray area like gambling, or what if most investors have already invested in competitive products?)

Can customers be acquired profitably? (What if customers are willing to pay $5k/year for 5 years, but it takes $30k of sales and marketing effort to acquire each customer?)

Are there enough potential customers to generate hundreds of millions in annual revenue? (What if the target market is smaller than the founder thinks, or if it doesn’t grow as quickly as anticipated?)

.. and so on..

Some of these risks can be addressed very quickly. For example, if a founding team has worked together before, then the chance of a team break-up is small. If the founders have individual histories of shipping great products, then they’ll probably do a good job with their next product, too.

Other risks require more time and effort. Will customer acquisition costs be reasonable? Will a founder who has never done recruiting be good at it? These questions are hard to answer until a company actually tries acquiring customers or recruiting new employees.

Every startup has a different bundle of risks, and it’s important to address the most dangerous ones as quickly and cheaply as possible. The Lean Startup movement is built around this principle: for most companies, being able to build a product is straightforward, but building the right product is not, so the early days of a company should typically be spent doing customer development instead of writing code.

The relationship between risks and valuations

If two best friends just incorporated a company and investors are offering to invest at a $5m valuation, has $5m in value already been created?? LOL. No.

In the early days of a company, valuations are based on what the company might accomplish (potential energy), not what it’s actually accomplishing (kinetic energy). How do investors assign a value to the company’s potential? They guess. They estimate the best possible outcome and then weigh that against the company’s bundle of risks.

For example, maybe Americans spend $1b annually on some widget, and a startup has a plan to sell a better version of that widget for 50% of the price. Let’s say in the best case scenario, this company will eventually sell $500m of widgets each year with a 40% margin. Applying NASDAQ’s 25x price/earnings ratio to an annual profit of $200m ($500m * 40%) yields a market cap of $5b. That’s the best case scenario – a complete monopoly over the widget market.

Next, an investor will start discounting that $5b valuation based on a startup’s risks. Maybe the team lacks manufacturing experience, so there’s a 30% chance their manufacturing plan will fail. And the founders just met, so there’s a 40% chance they’ll break up within a year. And the CEO doesn’t seem like a great recruiter, so there’s a 60% chance the founders won’t be able to build out an adequate team. Also, consumers can be unpredictable, so there’s an 85% chance that even if the company builds an awesome widget, they won’t be able to get significant traction in the market. Finally, there’s a 75% chance that the widget will be copyable and that competition will drive margins to approximately 0%.

All of these risks mean that the “expected value” of this company is $5b * 70% * 60% * 40% * 15% * 25% = ~$32m. If an investor is targeting a 4x return, then $8m would be a fair valuation to propose. (At that valuation, the expected ROI would be 4x.)

Do investors really think like this? Oftentimes yes, but more qualitatively than quantitatively. Will margins be 40% or 35%? Is the likelihood that a team will break up 40% or 60%? No one really knows. So investors use their gut to categorize risks as low, medium, or high. The more high risks there are, the lower a company’s expected value. The actual logic might sound something like: “A typical seed valuation these days is $5m. The founders recently met, so the probability of a founder split is higher than usual. However, the CEO is a successful serial founder, so there’s a much higher chance that she can recruit and manage effectively (and it’s more likely she could survive a founder split). Also, the CMO is amazing, so the likelihood of successfully marketing to consumers is much higher than usual. Taking all of these factors into account, the valuation should be a little higher than $5m. Maybe $7m or so.”

In essence, a company’s valuation is based on its ideal outcome, weighed by the likelihood of overcoming all of its risks. The best way to grow the valuation is to mitigate the biggest risks.

Two Common Mistakes When Addressing Risks

Mistake #1: Using up resources to address minor risks

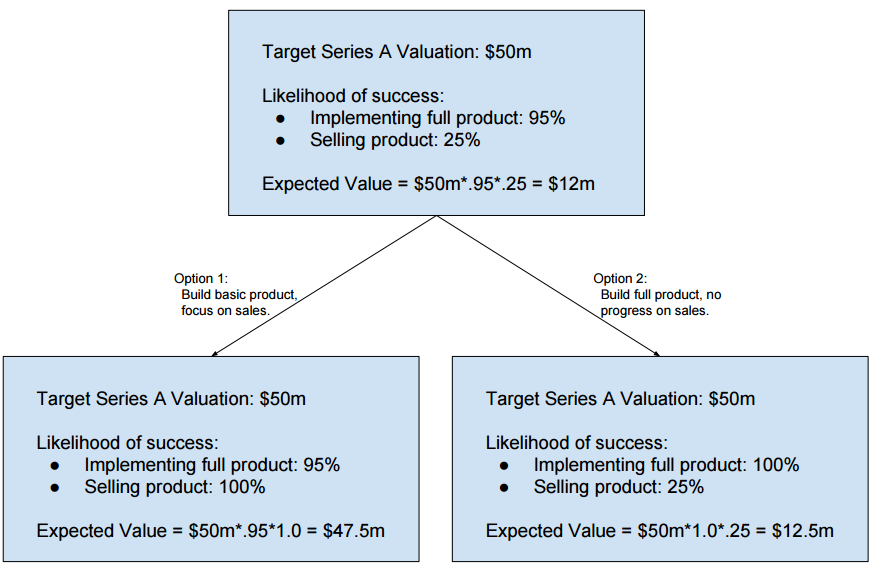

If investors are not worried about X, then seed capital should not be spent proving that they’re right not to worry. One common example of this mistake is a very strong technical founder spending all of their seed capital on writing code and building a product, but not launching or getting any customer feedback. From an investor’s perspective, a strong technical founder has a >95% chance of building whatever they set out to build, but maybe a 25% chance of being able to find product/market fit or being able to generate meaningful sales. Proving out the engineering side will bump up the .95 multiplier to 1.0, but proving out the sales side will bump up the .25 multiplier to 1.0 – a much bigger impact on a startup’s valuation. See the diagram below:

Mistake #2: Fundraising just after a major initiative fails

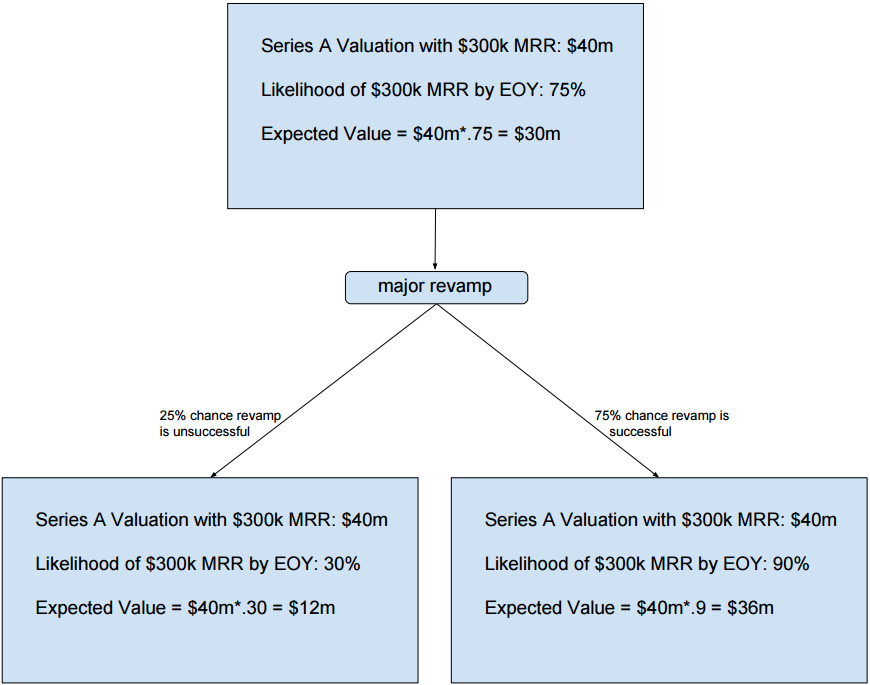

The best times to fundraise are 1) when your traction is great or 2) when you’re about to do something that might make your traction great. The worst time to raise is when you just tried something major and failed. The diagram below shows a product that’s about to undergo a revamp. There’s a 75% chance the revamp will boost revenue and a 25% chance it will hurt revenue. The best time to fundraise would be just before launch, or just after a successful launch. Raising after an unsuccessful launch is a terrible idea because your startup’s valuation will be much lower. (It’s ultimately up to the founder whether to raise pre-revamp at a slightly lower valuation, or to launch the revamp and risk a major valuation drop in exchange for a good shot at a higher valuation.)

Making progress can still lead to failure

Returning to the questions at the beginning of this post, the reason that founders often have a hard time raising a new round despite making progress since their previous round is because they didn’t address any significant risks. If a company’s seed round was based on the assumption that there was an 80% chance of X and a 40% chance of Y (where X and Y are both desirable), and the company used its capital to increase the likelihood of X to 90% while the likelihood of Y dropped to 20%, then the company’s expected value will be nearly halved despite “making progress.”

To avoid this trap, founders need to be aware of the major risks in their startups – both actual and investor-perceived – and address as many of these risks as possible with the capital on hand.